Market

October 13, 2016

Are Flat Rolled Steel Prices Poised to Move Higher?

Written by John Packard

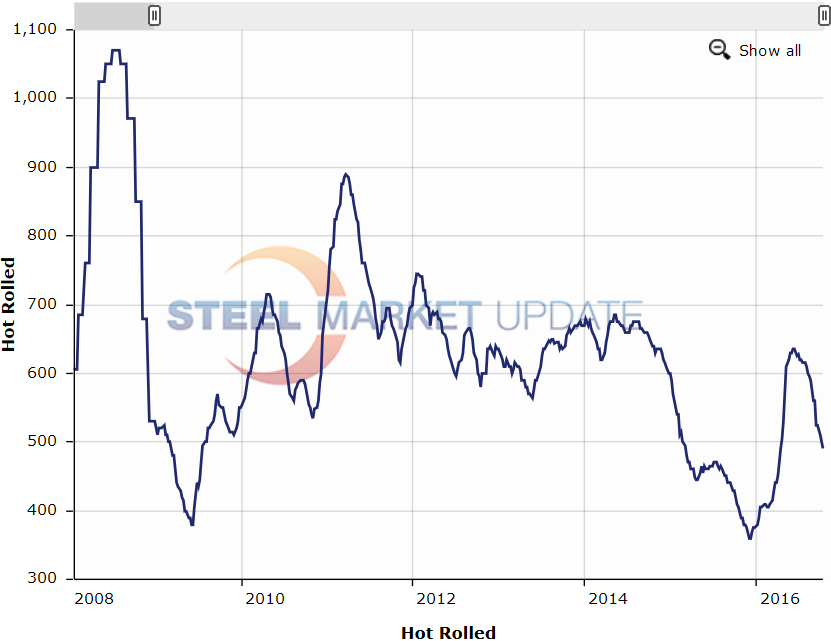

The conversation has begun regarding when flat rolled steel prices will end their slide and reverse course. Flat rolled steel prices have been in a steep decline since mid-June 2016 when benchmark hot rolled prices peaked at $635 per ton ($31.75/cwt, SMU index average) FOB domestic mill. Since then steel prices have retreated $145 per ton and HRC is currently averaging $490 per ton (SMU index).

There are some who believe prices are close to a “cycle” low while others are of the opinion prices will continue to drop from here.

The last cyclical low point was achieved the first week of December 2015 when SMU reported hot rolled coil as averaging $360 per ton ($18.00/cwt). This low was created after one of the longest losing streaks in recent pricing history as HRC went from $685 per ton in early May 2014 before sliding 19 months (we did have a dead cat bounce in there from April into July 2015) until the bleeding was stopped in early December 2015.

Going back to January 2008 there was only one other time when HRC prices bottomed under $400 per ton. That was in June 2009 at the peak of the Great Recession and even then prices bottomed at $380 per ton.

For that matter, prior to this week there have only been two times during the past 9 years when the HRC pricing cycle past through $500 per ton: 2009 and 2015.

On paper there are a number of items which should give the domestic mills some momentum to stop the price erosion soon. The domestic mills have been successful in controlling exports of foreign hot rolled from a number of countries and our sources are advising us there are few hot rolled offers into the U.S. market and those that exist are at price levels not too distant from the current $490 per ton average we reported earlier this week. We heard from one of the Turkish mills that they are out of the U.S. market right now because of increasing pricing in their home market. We expect this is probably true in other countries as well. So, we have limited foreign supply to pressure U.S. prices.

US Steel Granite City and Fairfield steelmaking mills are not running and there is no indication that they will run anytime soon. At the same time AK Steel Ashland blast furnace is also off-line. The only steelmaking coming back online is the blast furnace at ArcelorMittal Indiana Harbor, a portion of which will be used as a slab source for AM/NS Calvert.

On top of this with POSCO being knocked out as a source of hot rolled supply to the USS/POSCO (UPI) joint venture mill has created an opportunity for US Steel to ship hot bands from its Midwest/Eastern mills. Our understanding is there are well more than 100,000 tons of hot bands on order with USS heading for UPI. The UPI mill uses 70-90,000 tons per month of HR feedstock. With Vietnam being eliminated from the West Coast market both CSI and UPI should be running at capacity. This means USS (at least for the short term) has a large hot rolled customer that was much smaller a few months ago.

On the flip side we have Big River Steel coming online having advised at our 6th Steel Summit Conference that the mill is open for HR business taking orders for December production. We anticipate that the early order book will not be enough to challenge the surrounding mills. Once we spill into First Quarter 2017 that may very well change. So, for the moment, we see the domestic mills as continuing to control domestic supply – especially on hot rolled coil.

Ferrous scrap prices continued their slide as October negotiations between the steel mills and their scrap suppliers come to a conclusion at the end of last week. Prices were down anywhere from $15 to $30 per gross ton. As scrap prices weaken it allows the EAF (electric arc furnace) domestic mills to lower prices while keeping margins essentially the same. With Busheling (which is a major scrap input used by sheet mills) around $210 per gross ton in the Midwest and shredded just below it around $200 per gross ton if we use a simple +$150 per ton conversion cost (and Mark Millett of SDI told our Steel Summit audience that their cost is “well below” the $150 number) we conservatively generate a hot band cost of $360 per ton. So, there is still plenty of room for prices to fall should an EAF mill decide they want a piece of spot business. As of this week the lowest price we have picked up in the market was $440 with more transactions coming in at $460 and $480 per ton. So, our opinion is there is more room to move at least out of the EAF “mini” mills.

However, we believe scrap prices will settle at these levels and then slowly rise as we head into the winter months. If that turns out to be correct that would be a precursor to steel prices rallying and setting a bottom for benchmark hot rolled as well as cold rolled and coated.

Demand continues to be a question mark when it comes to hot rolled with energy, agricultural equipment, mining all being major uses of hot rolled and all being at the low points of their business cycles.

We are hearing demand on automotive and construction continue to be good which is supportive of cold rolled and coated pricing.

Last week we asked those participating in our flat rolled steel market trends analysis what they thought regarding the direction flat rolled steel prices will trend over the next 30 to 60 days. We had 67 percent of the respondents report prices would go lower (down from 73 percent two weeks earlier). Only 3 percent believe prices would go higher from here. A note to our readers, history shows the steel buyers are sometimes the last ones to figure out a price increase is coming so we don’t hold a lot of confidence in this response level.

We prefer to look at what is happening with service center spot prices and the comments that we are getting to see if the distributors have reached critical mass (which we call capitulation). Capitulation is that point in time when 75 percent or more of the service centers responding to our survey report their company’s spot resale prices as falling. True capitulation comes when those lower spot prices create margin compression (or losses). When that happens, the distributors want the mills to raise prices which they will support in order to improve the value of their inventories.

Besides capitulation at the service centers, what are some of the other “early warning signs” that prices may soon reverse course?

Lead times on cold rolled and coated begin slipping into January and hot rolled lead times are into December. As lead times move into 1st Quarter there tends to be a pent up demand for inventory both in contracts and spot inventories at service centers.

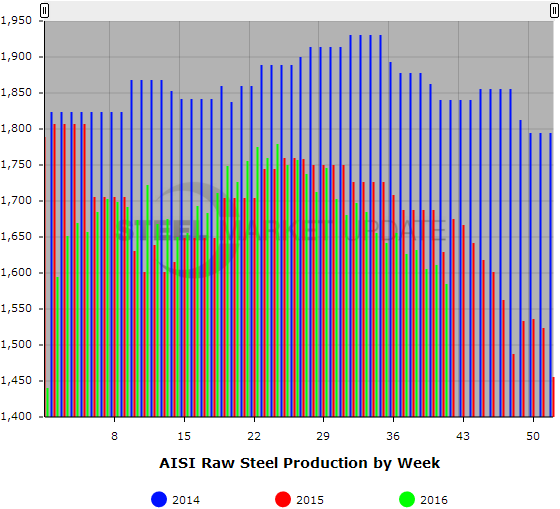

Stronger lead times should also mean an increase in raw steel production. You can see how production has dropped off over the past three years according to the weekly raw steel production report from the American Iron and Steel Institute (AISI).

Service center inventories become “tight” at less than 2 months supply. According to the MSCI cold rolled and coated are already at tight inventory levels. Our survey has flat rolled inventories at 2.26 months supply.

Plate price increase announcement(s) are made. Nucor announced a $30 per ton price increase on plate earlier this week. Over the past few sheet announcements they were preceded by plate price announcements. However, none of the other plate mills have moved pricing in tandem with Nucor which shows us that the market is still too weak for an increase to hold.

Here is the opinion of one large service center chain about where they think prices will bottom, “…Last year, CRU HR averaged $412/ton in Oct, and averaged $364/ton in Dec, when it bottomed, or a monthly difference of $48/ton. Assuming we’re in a current market of around $490/ton, if we saw a similar drop before we bottom this year, it would be around $440/ton or so, and I think that’s as good a guess as any for now for calling a bottom range.”

The post Are Flat Rolled Steel Prices Poised to Move Higher? appeared first on Steel Market Update.

{kind=link}

{kind=link}