Market

June 30, 2022

Tanners: That Was Fun, But a “Sheet Storm” Is Brewing

Written by David Schollaert

The rally was fun while it lasted, but new capacity delayed in large part because of Covid has arrived or soon will, popular analyst Timna Tanners said.

And it will coincide with some demand weakness. The result: “steelmageddon” (aka “sheet storm”) might have been delayed. But it has finally arrived, she said.

“Here we are with capacity starting to ramp up. The market is seeing a lot more supply in an environment (in which) I am not convinced that there is going to be more demand,” Tanners said.

A managing director at Wolfe Research, she made the comments during an SMU Community Chat on Wednesday.

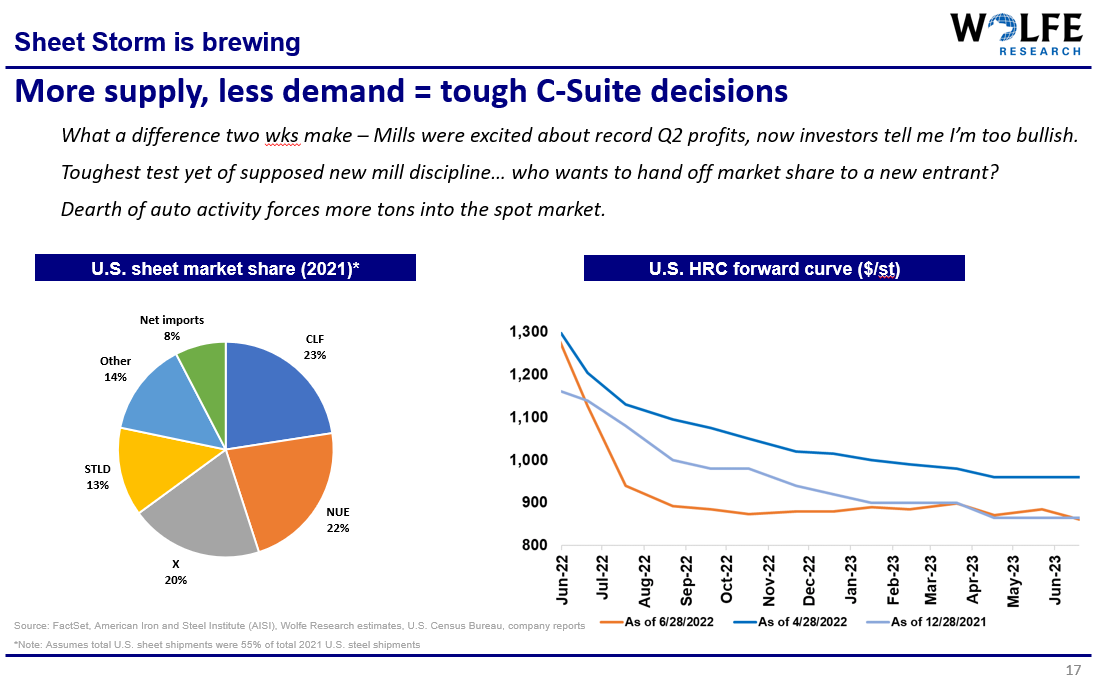

The dynamic of added capacity and sliding demand is already causing prices to correct from recent highs. And it’s not clear where the bottom is. The downside risk to iron ore and met coal could send global prices lower, pushing US prices down another $100-300 per ton from current levels. (See chart below, and click to enlarge.)

Tanners also underscored the tension inherent in the current market. Namely, a “fascinating test of supposed mill discipline – when there’s good money to be made, and shutting domestic capacity means handing market share to a competitor.”

With selling prices still well above conversion costs, profitability itself could be one of the main drivers of price erosion. Why should mills cut capacity when they’re still making money? Assuming conversion costs settle somewhere around $250 per ton (higher than in the past because of cost inflation), Tanners expects EAF mills are still firmly in the black until roughly $700 per ton.

Currently, the only significant tonnage offline is at Cleveland-Cliffs, which has not restarted the C-5 blast furnace at its mill in Cleveland. The furnace, idled earlier this year for maintenance, was originally expected to restart in June. Lower-than-expected auto industry demand might not justify that capacity coming back online now, Tanners said.

Cliffs did not respond to a request for comment from SMU about the status of the C-5 furnace. A company spokeswoman told SMU on June 21 that rumors about anything besides a planned outage on C-5 was “speculating and not accurate.”

Even if there are no confirmed blast furnace idlings,”utilization rates have pared back a bit recently – an indication of slack demand,” Tanners said. She noted that EAF mills can quietly scale back production without the attention that comes with idling a blast furnace.

Tanners also questioned how long prime scrap might remain the next precious metal. More alternatives to prime will be available in the coming years, especially as North America mills become more vertically integrated with, for example, their own pig iron and direct-reduced (DRI) iron capacity.

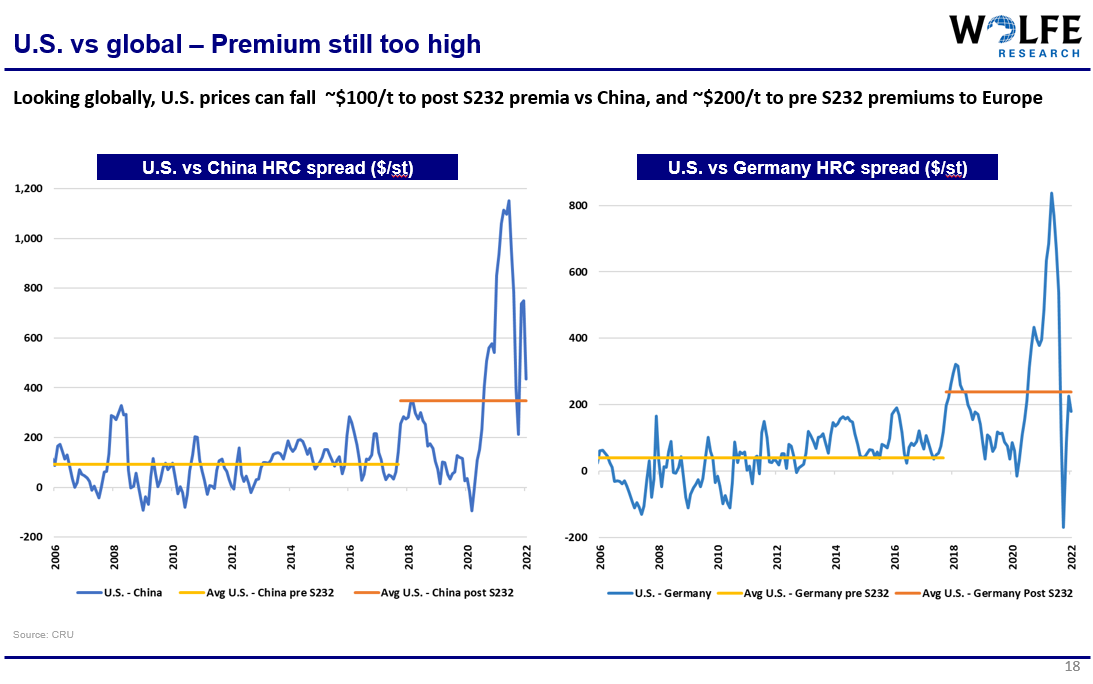

Also, US prices are still high versus those abroad, which means domestic prices still have further room to fall. (See chart below. Click to enlarge.) It is also possible that high levels of low-priced exports from China and Russian could continue to drive down Asian prices, indirectly keeping pressure on tags elsewhere as well, she said.

In the near term, mills continue to insist on strong underlying demand. Nonresidential construction and energy all have upside. And mills are particularly bullish on infrastructure. But that is mostly a driver for rebar demand and less so for sheet, Tanners said.

Some late summer disruptions are possible, especially should labor negotiations turn contentious at US Steel, Cleveland-Cliffs, Algoma, or Stelco. All of this, though, “would only support prices in the near term. In the long-term, new capacity is arriving. But unfortunately, it coincides with some demand weakness,” Tanners said.

And that doesn’t include the possibility of a potentially prolonged recession that could stifle activity and lead service centers to hold less inventory, she added.

Editor’s note: Missed the Community Chat with Timna Tanners? No problem. Click here for a recording of this and past SMU webinars.

The next SMU Community Chat will feature Anton Posner, CEO of Mercury Resources LLC, on July 13 at 11am ET. Click here to register.

By David Schollaert, David@SteelMarketUpdate.com

The post Tanners: That Was Fun, But a “Sheet Storm” Is Brewing appeared first on Steel Market Update.

{kind=link}

{kind=link}