Market

February 4, 2014

SMU Price Momentum Adjusted & SMU Price Indices

Written by John Packard

On January 14, Steel Market Update (SMU) adjusted our Price Momentum Indicator from Higher to Neutral. This means we see steel market pricing at this moment as either in transition or moving sideways over the next 30 days. With ferrous scrap prices now weakening, lead times shortening and all of the available capacity back in the market the chances of steel prices remaining the same or moving slightly lower outweigh the chances that they will move higher from here. SMU last moved our Indicator from Neutral to Higher on October 31, 2013.

Market prices continue to be in a fairly tight range and the domestic mills are attempting to hold the line. Even so, we are starting to see some cracks in the armor as lead times – especially on hot rolled coils – are starting to pull back. We have heard of a number of mills looking for business – not giving it away mind you – but looking for orders on hot rolled, cold rolled and coated products. At the same time one of the coating mills was complaining to Steel Market Update of the impact foreign steel was having on their order book.

We are receiving mixed messages regarding demand for flat rolled steel products since the start of the New Year. We have also received mixed messages regarding flat rolled steel pricing – more specifically hot rolled steel pricing – since the year began. During the later parts of January SMU became aware of a couple of mills lowering their offer prices on hot rolled into the spot market. The buyers were telling us at the time that lead times were short on the product and a couple of mills were interested in tonnage in order to keep their books filled.

In the beginning of January SMU received a note from a large manufacturing company who purchases hot rolled steel in the spot market. He indicated the offers which were at $700 per ton the first week of January had dropped since then. Even a couple of the integrated mills told this one buyer that the $700 number was negotiable with “tons.”

The manufacturing company went on to speak about lead times which are critical to keeping market prices up, “Mills are shipping early or right on time, everyone needs tons and no one in their right mind should be paying a penny over $680 today. I think we hit the peak in the last week in December and, as long as scrap behaves, the price is going to start to slide, albeit very slowly, for the next few weeks. The only thing holding this together is very strict pricing discipline. AK is behaving for now, and the TK guys are scared to death of upsetting their soon to be new handlers. At the same time tepid business conditions and the possible influx of imports in the next few weeks, doesn’t bode well for order books and lead times.”

From the east coast we gathered an earful regarding demand, the impact of foreign steel and mill pricing:

“The conditions in the Northeast region are dynamically different than the rest of the country. Market conditions remain flat. Lots of ups and downs, no rhythm. Busy many days and then you are checking to see if your telephone is working.

“The crux of the marketplace has to be the foreign suppliers. There are more countries offering steel, today, than we have seen in a very long time. And then there are multiple mills within some countries. An example would be China, who has three mills offering steel to the east coast.

“Domestically, the pressure is for additional increases, which we have not been able to pass on to the marketplace. I believe the domestic mills have had trouble in passing these increases on to the east coast, due to the level of foreign incoming steel. Domestic lead-times, which increased in late October, seem to have calmed. Domestic pricing, for the most part, is exactly what you have published in your SMU. We have reached the $700/ton level for Hot Rolled, which I thought would be a reach. No one is asking for an order, but that is somewhat standard. The domestic suppliers have less and less staff available to the consumer….” This service center executive went on to point out that the foreign prices were beginning to rise and that would be helpful in drying up position (unsold) tons sitting on the docks and put more risk on trading companies to import material without a firm order against it.

In the Midwest offers on hot rolled coil which were at $690 with $680 being “doable” at the beginning of January dropped to $640 with $660-$670 being the every day price by the end of the month.

One mid-sized service center executive informed SMU they had been offered $38.00/cwt base cold rolled. “If we are getting it others are getting $38 as well.”

From the South Central U.S. we heard from a large service center group, “I think the highest price being quoted is moving to $34 (including Severstal), so certainly not a collapse or anything, but it is a change lower, from the last number of weeks. I’m just going to be curious if the CRU average begins to move down due to a) more volume booked last week vs. the prior, b) mills backing off of last increase, and trying to hold onto $34. If $34 becomes or is the high end, what will the average become?”

This same service center provided SMU with information regarding demand within their customer groups:

“Our area experienced 10% volume growth in ’13, driven mostly by Commercial Equipment, Transportation, and Fabricators. The outlook from the same basket of customers is very positive for 2014, with continued stability and growth, but at a lower growth % in ’14. For whatever its worth, this year so far has started slower than anticipated. We’re chalking it up to post-holiday sluggishness and hope to see activity ramp up quickly. Besides the industries mentioned, we’re seeing some anecdotal increased Construction-related inquiries/sales in the last 90 days or so, and we believe that will continue. We are penciling in around a 2-5% growth rate factor for 2014. If we had greater exposure to Construction, it would be higher.”

Another large service center told us, “…truck trailer is above the trend of other industries, and the lead time to buy a trailer exceeds the lead-time to buy the tractor. Otherwise, demand is mainly neutral.”

This service center went on to say, “Regarding the increase to a published $700; When mills are willing to publish an actual price (rather than an increase amount), it means that no one in their open order book is paying the new published price. Obviously, if somebody was paying $700 and saw the report of an increase to $700 that customer would be ‘disappointed’. We are not seeing much strength in prices and lead-times, but mills still are keeping the discipline of not moving backwards. Lots of prices out there, for economic mill quantity orders are transacting at pricing around $630 – $665 depending on total size.”

We heard during our conference call with HARDI members that galvanized prices were being transacted at numbers available prior to the Christmas price announcement. That would put the base price numbers in the $38.50/cwt-$39.50/cwt range rather than $40.50/cwt.

However, one of the coating mills told SMU today prices continue to be “firm.”

As we have mentioned in the past, there appears to be a disparity between the “haves” – those mills associated with automotive, and the “have-nots” – those mills who are more construction related. The biggest disparity in pricing may well be the automotive coating lines and those of the construction mills.

Even so, we heard of one of the automotive mills needing galvanized orders. Speculation was the need could be related to a slowdown in production on a specific auto or truck model.

We are also hearing that imports are impacting the Galvalume market – especially in prepainted steel and in the South. This is one product where we have seen lead times (as reported by the mills to their customers) having moved in from what were once extended lead times.

Steel Market Update is NOT forecasting a collapse of the existing price structure. We will have to wait and see if demand rebounds after the cold weather of this past week. As one service center put it to us earlier today, “The weather has effected demand much more than supply.”

Our expectation is for prices to move sideways to slightly lower over the next 30 days.

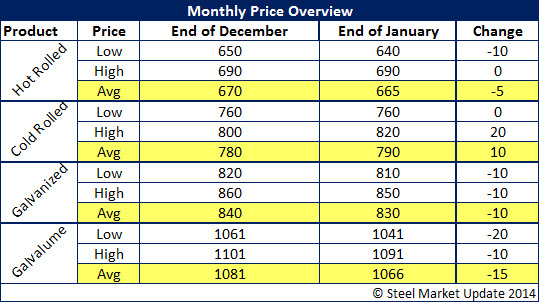

Here is how Steel Market Update saw prices during the month of January:

The post SMU Price Momentum Adjusted & SMU Price Indices appeared first on Steel Market Update.